Cloud Infrastructure Spending Continued to Grow in 2Q23, According to IDC

According to IDC, spending on compute and storage infrastructure products for cloud deployments increased 7.9% year over year in 2Q23 to $24.6 billion.

Spending on cloud infrastructure continues to outgrow the non-cloud segment with the latter declining 8.3% in 2Q23 to $14.4 billion.

The cloud infrastructure segment experienced a decline of 23.2% in unit demand with an increase in average selling prices (ASPs), mostly related to higher than usual GPU server shipments to hyperscalers.

According to the International Data Corporation (IDC) Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, spending on compute and storage infrastructure products for cloud deployments, including dedicated and shared IT environments, increased 7.9% year over year in the second quarter of 2023 (2Q23) to $24.6 billion. Spending on cloud infrastructure continues to outgrow the non-cloud segment with the latter declining 8.3% in 2Q23 to $14.4 billion. The cloud infrastructure segment experienced a decline of 23.2% in unit demand with an increase in average selling prices (ASPs), mostly related to higher than usual GPU server shipments to hyperscalers.

Juan Pablo Seminara, research director with IDC's Worldwide Enterprise Infrastructure Tracker

"Cloud infrastructure spending is shifting towards robust configurations geared towards more complex workloads and new AI initiatives," said Juan Pablo Seminara, research director with IDC's Worldwide Enterprise Infrastructure Tracker. "Despite the steep decline in system unit demand for the first half of the year, the spending outlook for 2023 remains positive with growth centered on the expectation that higher ASPs will remain for the rest of the year."

Spending on shared cloud infrastructure reached $17.9 billion in the quarter, increasing 13.7% compared to a year ago. The shared cloud infrastructure category has surpassed non-cloud spending in the first half of 2023 accounting for 45.8% of total infrastructure spending. The dedicated cloud infrastructure segment declined 4.9% year over year in 2Q23 to $6.7 billion. Of the total dedicated cloud infrastructure, 43.9% was deployed on customer premises during the quarter.

For 2023, IDC is forecasting cloud infrastructure spending to grow 10.6% compared to 2022 to $101.4 billion – a slight improvement from the prior outlook for the year of 7.3% growth. Non-cloud infrastructure is expected to decline 7.9% to $58.5 billion. Shared cloud infrastructure is expected to grow 13.5% year over year to $72.0 billion for the full year, while spending on dedicated cloud infrastructure is expected to grow 4.1% to $29.4 billion for the full year. The subdued growth forecast for non-cloud infrastructure reflects the expectation that the market will face headwinds, but cloud spending will remain positive due to new and existing mission-critical workloads, which often require higher-end, performance-oriented systems.

IDC's service provider category includes cloud service providers, digital service providers, communications service providers, hyperscalers, and managed service providers. In 2Q23, service providers as a group spent $24.1 billion on compute and storage infrastructure, up 7.1% from the prior year. This spending accounted for 61.9% of the total market. Non-service providers (e.g., enterprises, government, etc.) decreased their spending 6.9% year over year. IDC expects compute and storage spending by service providers to reach $99.1 billion in 2023, growing 9.0% year over year.

On a geographic basis, year-over-year spending on cloud infrastructure in 2Q23 increased in all regions except Canada, Central & Eastern Europe (CEE), which was impacted by the Russia-Ukraine war, and Western Europe, where the effects of high energy prices and a tight macroeconomic environment are at the forefront of client spending decisions. Cloud infrastructure spending in CEE declined 15.2% year over year, while Canada was down 36.4% and Western Europe declined 3.5%. Cloud infrastructure spending in the USA, Japan, Middle East & Africa, Latin America, and Asia/Pacific (excluding Japan and China) (APeJC) grew 15.8%, 14.1%, 9.2%, 8.3%, and 2.8% year over year, respectively. China ended the quarter with growth of 0.1% year over year.

For 2023, cloud infrastructure spending is expected to grow in all regions except CEE and Canada, with Latin America expected to grow fastest at 18.4%. All other regions (APeJC, Canada, China, Japan, Latin America, USA, and Western Europe) are expected to post annual growth in the 0-13% range.

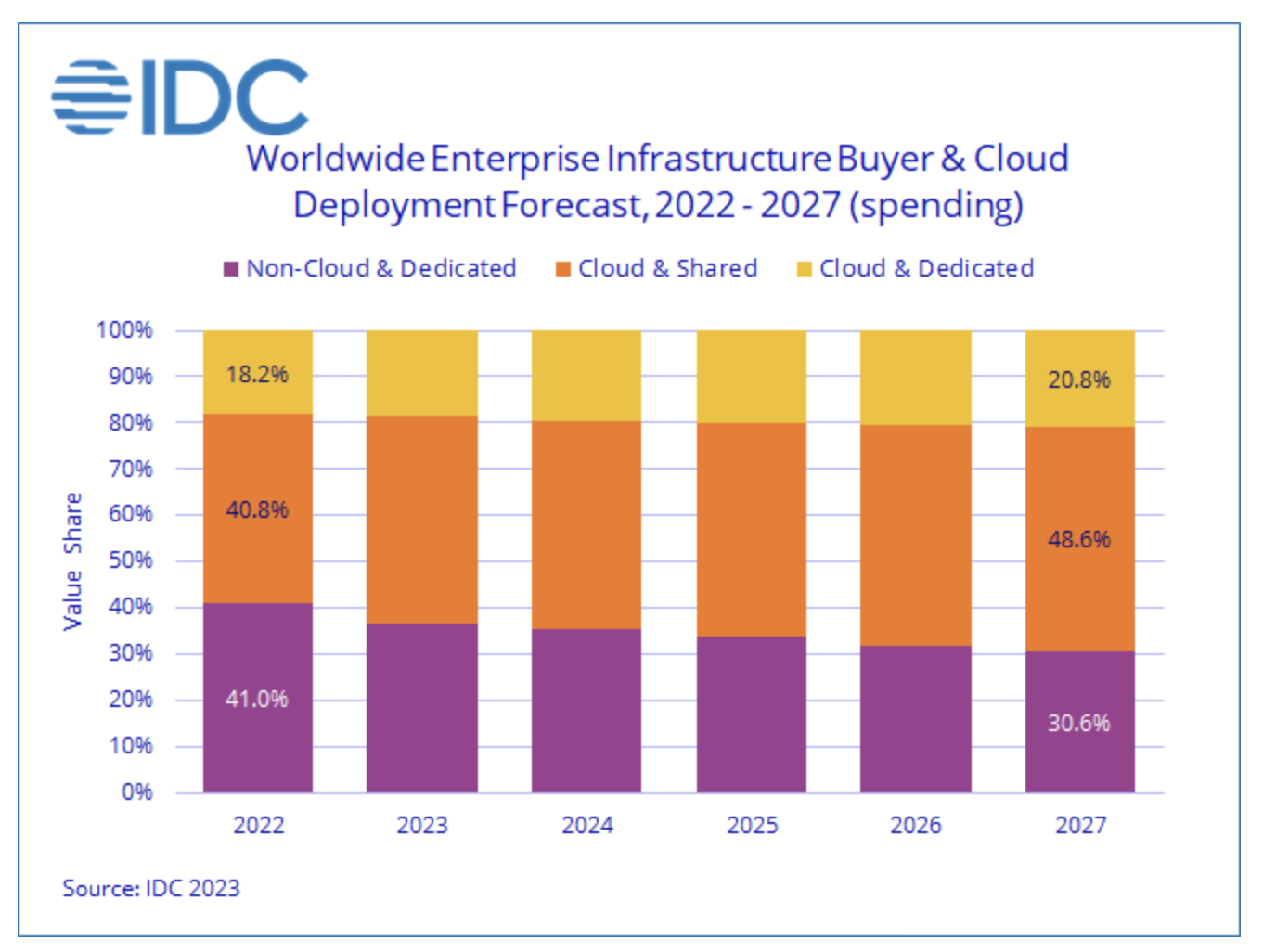

Long term, IDC predicts spending on cloud infrastructure to have a compound annual growth rate (CAGR) of 11.3% over the 2022-2027 forecast period, reaching $156.7 billion in 2027 and accounting for 69.4% of total compute and storage infrastructure spend. Shared cloud infrastructure spending will account for 70.0% of the total cloud amount, growing at a 11.6% CAGR and reaching $109.7 billion in 2027. Spending on dedicated cloud infrastructure will grow at a CAGR of 10.7% to $47.0 billion. Spending on non-cloud infrastructure will grow at 1.7% CAGR, reaching $69.1 billion in 2027. Spending by service providers on compute and storage infrastructure is expected to grow at a 10.9% CAGR, reaching $152.6 billion in 2027.

To read more, please visit www.idc.com.