Consumer Tablet Shipments Grow 19.7% in 2025, While Delays in Manifesto Deals Weigh on Overall Market – IDC – April 17, 2026.

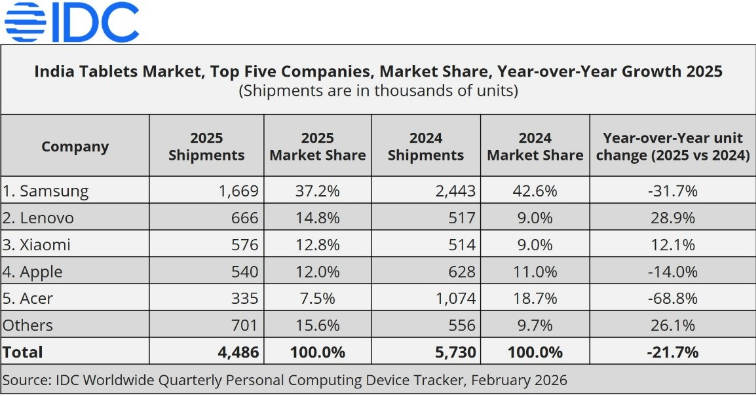

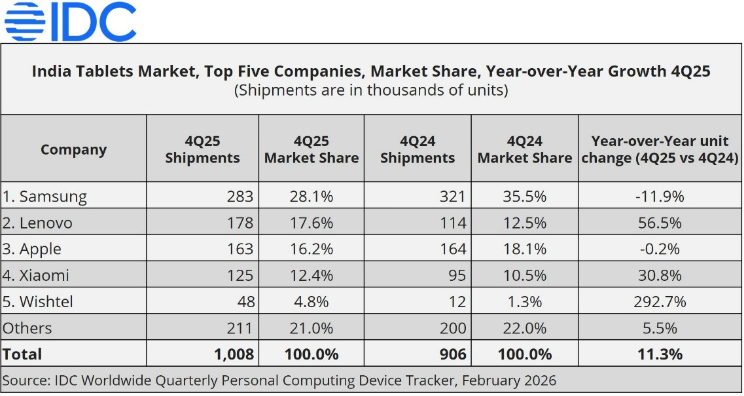

India’s tablet market—including detachable and slate tablets—shipped 4.49 million units in 2025, declining 21.7% year over year (YoY), as a sharp contraction in the commercial segment offset continued strength in consumer demand, according to IDC’s Worldwide Quarterly Personal Computing Device Tracker. While detachable tablets grew 20.1% YoY, a sharp 34.6% YoY decline in slate tablets weighed on overall market performance. Despite a decline in the first 3 quarters, the tablet shipments rebounded in 4Q25, growing 11.3% YoY, supported by stronger consumer demand despite continued weakness in the commercial segment.

Consumer and Commercial Segment Performance

Consumer Segment: Grew 19.7% YoY in 2025, driven by strong buyer demand, aggressive vendor sell-in, and sustained traction across e-commerce platforms and retail channels during seasonal sales. Consumer shipments further increased 27.1% YoY in 4Q25, highlighting continued resilience in the segment.

Commercial Segment: Declined sharply by 55.1% YoY in 2025 due to postponed manifesto deals and delayed government orders. The education segment fell 62.2% YoY, while government shipments declined 55.0% YoY. Commercial shipments remained weak in 4Q25, dropping 17.3% YoY.

Tiwari, research analyst at IDC

Market Trends

The gap between consumer and commercial performance reflects shifting demand dynamics. Consumer adoption remained strong, driven by entertainment, learning, and productivity use cases.

Commercial demand, however, was constrained by delayed institutional orders and budget pressures. Detachable tablets gained traction due to their hybrid functionality, whereas slate tablets faced increasing competition from PCs and smartphones, impacting overall market performance.

“Consumer demand strengthened through the year as vendors leaned into festive promotions, wider offline distribution, and feature-led differentiation,” said Priyansh Tiwari, research analyst, IDC India & South Asia. “The integration of 5G, AI-enabled productivity features, and smart note-taking capabilities is repositioning tablets beyond media consumption toward everyday productivity. As notebook prices rise, detachable tablets in particular are emerging as a practical, cost-effective alternative for students and young professionals.”

Top 5 Company Highlights: 2025

Samsung Electronics led the market with a 37.2% share, ranking first in both commercial and consumer segments with shares of 44.4% and 33.8%, respectively. The company’s dual-track strategy—leveraging large public education projects while sustaining strong online retail momentum—supported its market leadership. In 4Q25, Samsung captured a 28.1% share of the overall tablet market.

Lenovo secured second place with a 14.8% share, supported by strong consumer momentum, where shipments grew 55.6% year over year (YoY). The company expanded its presence across both commercial and consumer segments by strengthening enterprise engagement while broadening its consumer portfolio. In 4Q25, Lenovo captured a 17.6% share of the overall tablet market.

Xiaomi ranked third with a 12.8% share, benefiting from strong festive e-commerce demand and a refreshed value-for-money portfolio. By offering competitive hardware at aggressive price points, the company strengthened its appeal among student and youth segments. In 4Q25, Xiaomi held a 12.4% share of the overall tablet market.

Apple Inc. ranked fourth with a 12.0% share, supported by strong demand for its M-series iPad Pro and iPad Air models. Student-focused “Back to School” campaigns and attractive financing options helped the brand appeal to aspirational youth and creative professionals. Despite intensifying competition from Android vendors, Apple’s integrated ecosystem and focus on premium productivity continued to drive adoption across both consumer and enterprise segments. In 4Q25, Apple captured a 16.2% share of the overall tablet market.

Acer Group stood fifth with a 7.5% share, supported by fulfilment of large education manifesto deals and public sector projects. Despite softer government demand, the company sustained momentum through enterprise deployments and multinational accounts with its productivity-focused portfolio. In 4Q25, Acer held a 3.4% share of the overall tablet market.

“Consumer demand is expected to remain resilient, supported by media consumption and mobile productivity use cases,” said Bharath Shenoy, research manager, Devices Research, IDC India, South Asia & ANZ. “However, rising component costs could accelerate premiumization and slow replacement cycles at the entry level. As notebook prices firm up, detachable tablets bundled with keyboards and stylus are likely to gain traction as cost-effective productivity devices. In the commercial segment, budget constraints may also drive a gradual shift toward tablets in manifesto-led procurement.”

To learn more, visit: www.idc.com