Worldwide Smartphone Market Grows 2.3% in Q4 2025, Driven by Strong Performances from Samsung and Apple – IDC – March 05, 2026.

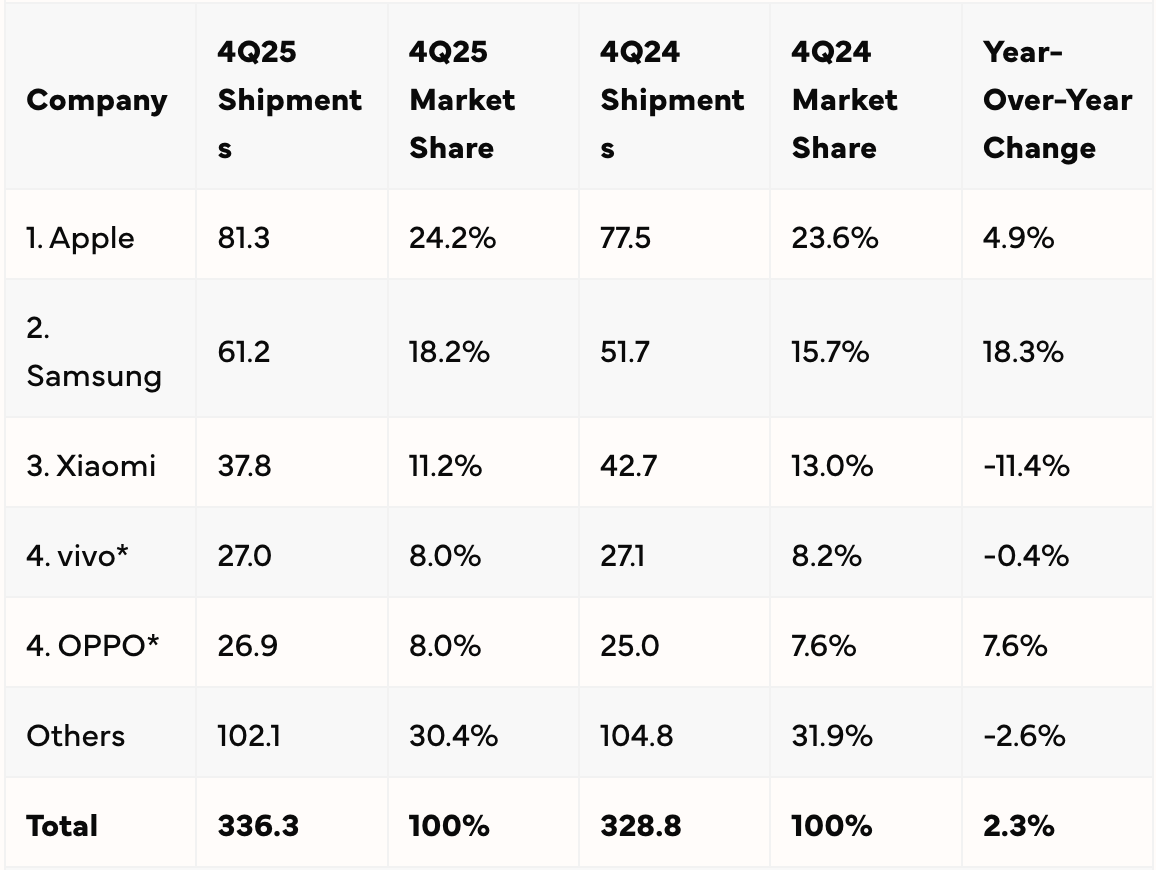

According to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, global smartphone shipments increased 2.3% year-over-year (YoY) to 336.3 million units in the fourth quarter of 2025 (4Q25). Despite the memory shortage crisis in Q4 2025, the market was supported by sustained premium growth, strong momentum in foldables and accelerated pull-in demand as consumers anticipated upcoming price hikes. The total number of smartphones shipped reached 1.26 billion units in 2025.

“Despite a challenging year marked with tariffs volatility, supply chain disruption and persistent macroeconomic headwinds across several markets, the global smartphone market demonstrated remarkable resilience, closing 2025 with a solid 1.9% year-over-year growth,” said Nabila Popal, senior research director for Worldwide Client Devices, IDC. “Interestingly, premium vendors Apple and Samsung were the primary growth drivers, posting the highest growth rates amongst the Top 5 at 6.3% and 7.9%, respectively. Apple maintained its leadership for the third consecutive year, achieving record-high shipments and a strong rebound in China fueled by the success of the iPhone 17 series. Even more notable, Apple and Samsung’s combined share expanded by two percentage points to 39%, up from 37% last year—underscoring the accelerating premiumization trend as consumers increasingly gravitate toward higher-end devices.”

Nabila Popal,

“Samsung delivered its strongest Q4 growth since 2013, driven by strong sales of its Galaxy Z Fold 7 and affordable AI-enabled Galaxy A-Series devices, while Apple achieved its best fourth quarter since 2021 and delivered the highest ever revenue in a single quarter, a strong testament to the success of the iPhone 17 lineup,” said Francisco Jeronimo, vice president for Worldwide Client Devices, IDC. “Overall, Q4 2025 was a remarkable quarter for both Apple and Samsung, as they consolidated their positions in the smartphone market by driving strong sales in the premium segment and reaching all-time high average selling prices (ASP).”

As the smartphone market shifts towards higher price points, most vendors continue to face intense pressure. Despite this, Xiaomi, vivo, and OPPO largely retained their market positions in 2025, with only marginal share losses. Xiaomi maintained its third position for the quarter and year, despite double digit decline in Q4, stemming from challenges of transitioning its portfolio toward higher price points and increased competition in China. Vivo remains heavily reliant on India, which was the primary driver for its growth. OPPO delivered a stronger Q4, supported by new product launches and strong performance in China, although its full-year performance was constrained by softer demand outside China.

“While 2025 was a positive year for smartphones, the industry is now facing a distinctly different outlook. The memory shortage, which is widely considered an unprecedented supply chain disruption, will cause the market to decline in 2026, and the duration of the shortage will ultimately determine the extent of the market contraction,” said Ryan Reith, group vice president for Worldwide Client Devices at IDC. “This is a time where the size and scale the OEM will be critical, as larger players will be better able to secure advantageous supply and workable price points. Despite the outlook being down, ASPs are expected to rise because of cost increases.”

Top 5 Companies, Worldwide Smartphone Shipments, Market Share, and Year-Over-Year Growth, Q4 2025 (Preliminary results, shipments in millions of units)

Table Notes:

Data are preliminary and subject to change.

Company shipments are branded device shipments and exclude OEM sales for all vendors.

The “Company” represents the current parent company (or holding company) for all brands owned and operated as a subsidiary.

Figures represent new shipments only and exclude refurbished units.

*IDC declares a statistical tie in the Smartphone market when there is a difference of one-tenth of one percent (0.1%) or less in the shipment shares among two or more companies.

To learn more, visit: www.idc.com