Asia/Pacific AI and GenAI Spending to Reach $370 Billion by 2029, Growing 5x – IDC – April 28, 2026.

According to the IDC’s Worldwide AI and Generative AI Spending Guide, AI and generative AI (GenAI) spending in Asia/Pacific, including China and Japan, is projected to grow from $73 billion in 2024 to $370 billion by 2029, representing a fivefold increase at a compound annual growth rate (CAGR) of 38.4%. GenAI is the fastest-growing segment, expected to reach approximately $175 billion by 2029 at a 68.2% CAGR, making up nearly half (47.4%) of all AI spending in the region. This growth signals a shift from early adoption to enterprise-wide operationalization of AI.

What is happening in the Asia/Pacific AI and GenAI market through 2029?

Vinayaka Venkatesh

Senior Market Analyst, IDC

AI and GenAI spending in Asia/Pacific is accelerating rapidly, with total investment expected to reach $370 billion by 2029. Growth is driven by enterprise demand for scalable infrastructure, operational efficiency, and AI-enabled applications, while challenges around governance, cost, and integration continue to shape adoption.

Key Market Metrics: Asia/Pacific AI and GenAI Market

Total AI and GenAI spending: $370 billion by 2029 (from $73 billion in 2024)

CAGR (2024–2029): 38.4%

GenAI spending: $175 billion by 2029

GenAI CAGR: 68.2%

GenAI share of total AI spending: 47.4%

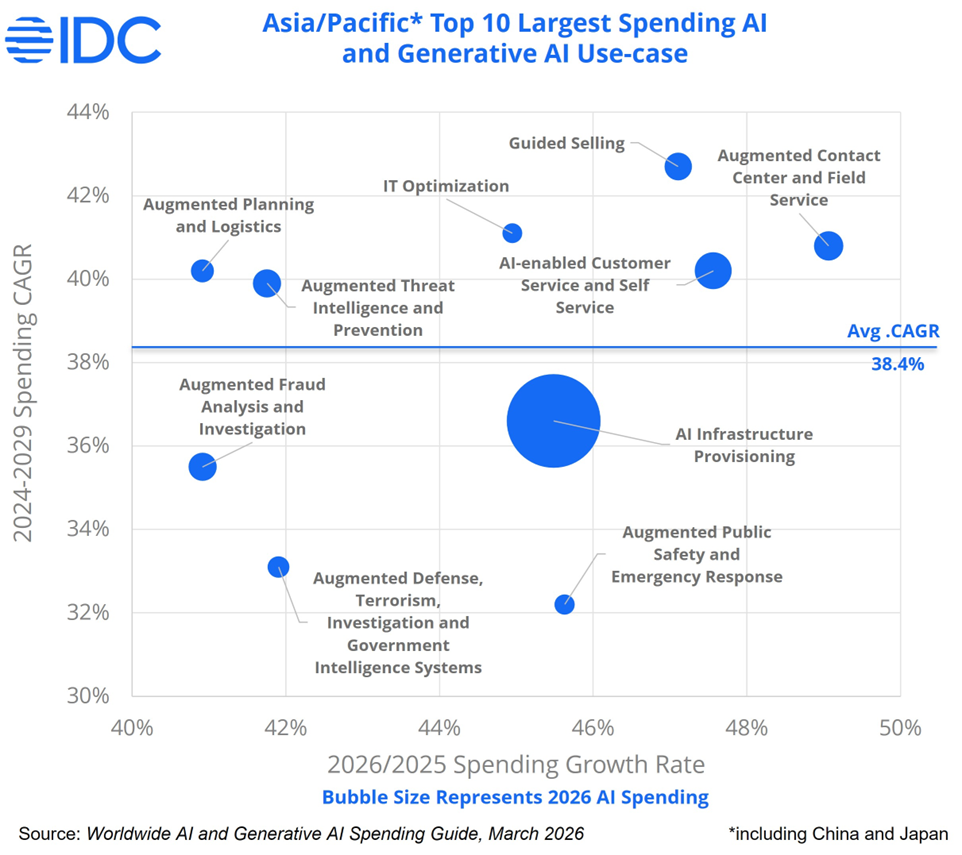

Leading use case: AI infrastructure provisioning (approximately 39% of total spending)

“The Asia/Pacific AI market has shifted from an infrastructure-building phase to one defined by platform consolidation and operational depth,” says Vinayaka Venkatesh, senior market analyst, Data & Analytics, IDC Asia/Pacific. “Organizations are prioritizing AI platforms that unify generative, predictive, and prescriptive capabilities, with increasing focus on AI agents and orchestration to scale enterprise-wide adoption.”

Why did the market change?

Growth is being driven by a convergence of enterprise priorities. Organizations are investing in AI to support increasingly complex workloads, deliver hyper-personalized customer experiences, and improve operational efficiency. At the same time, rising demand for real-time analytics and security intelligence is reinforcing AI as a core capability rather than a discretionary investment.

Agentic AI is also reshaping the market. Enterprises are embedding autonomous capabilities into applications and platforms, enabling AI systems to move from assisted decision-making toward more autonomous execution across workflows.

IDC Outlook

IDC expects continued strong growth as organizations move from isolated AI use cases to integrated, enterprise-wide AI ecosystems. Investment will increasingly shift toward platforms that support orchestration, governance, and scalability. However, challenges related to cost control, regulatory compliance, and skills availability may moderate the pace of adoption in some markets.

Industry Adoption Trends

AI adoption across Asia/Pacific is expanding in both depth and scope. The software and information services sector remains the largest contributor, accounting for more than 47% of AI spending in 2026, driven by investments in development platforms, training infrastructure, and intelligent applications.

Financial services continues to scale AI usage beyond traditional risk and fraud applications into autonomous advisory, compliance automation, and real-time decisioning. Telecommunications and retail are embedding AI into core operations, including predictive network management, intelligent customer routing, demand forecasting, dynamic pricing, and personalized commerce.

Use Case and Public Sector Momentum

AI infrastructure provisioning remains the largest use case, reflecting sustained investment in accelerated computing, cloud-native services, and data center capacity. At the same time, conversational AI and virtual assistants are evolving toward context-aware, multi-turn interactions that support self-service at scale.

In the public sector, AI is gaining traction in national security and emergency response. Governments are deploying AI for surveillance, predictive threat detection, and real-time data fusion to improve situational awareness and crisis response outcomes.

To learn more, visit: www.idc.com