Samsung and Apple Grew in Q1 2026 as Global Smartphone Shipments Decline 4.1% amid memory constraints – IDC – April 29, 2026.

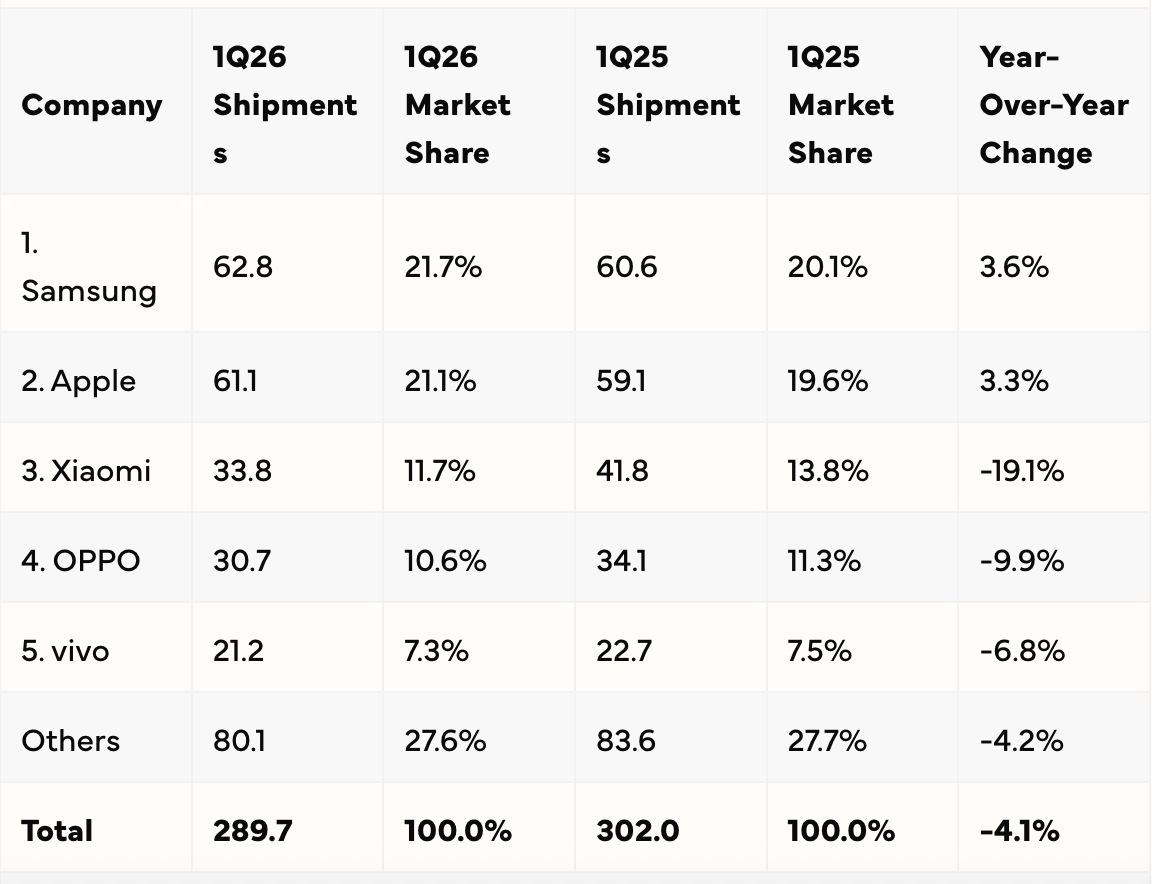

According to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, global smartphone shipments decreased 4.1% year-over-year (YoY) to 289.7 million units in the first quarter of 2026 (1Q26). This broke the 10 consecutive quarters growth streak that the market had seen since mid 2023. We expect the first quarter slowdown to be a mild precursor for what lies ahead in 2026 as the supply constraints around memory and price increases further dampen the market growth.

“The smartphone market has entered one of its most challenging periods, driven by acute memory supply constraints that are directly impacting both shipments and demand,” said Nabila Popal, senior research director for Worldwide Consumer Devices, IDC. “Limited memory availability is forcing shipment reductions, while sharply higher memory prices are pushing up bill‑of‑materials cost and forcing price hikes by many top brands. In several emerging markets, prices have risen by as much as 40–50%, significantly weighing on demand in price‑sensitive regions. Original equipment manufacturers (OEMs) are responding with tighter cost controls, reduced marketing and channel support, and increased use of despecing strategies—but such measures also limit growth. This calendar year represents a critical inflection point for vendors to reinvent themselves as rising component, energy, and logistics costs due to the recent war in the Middle East compound downside risks on the market outlook and pressure global smartphone demand.”

Nabila Popal, senior research director for Worldwide Consumer Devices, IDC

Who were the Top 5 Smartphone Companies in Q1 2026?

Despite the current market challenges, Samsung and Apple—the two leading companies—were also the only two companies in the global top five to register a YoY growth. Their strong focus on premium and higher leverage with memory suppliers has them better positioned to manage this crisis and gain market share. As the smartphone market shifts towards higher price points to offset increasing bill of materials (BOM) costs, all vendors continue to face intense pressure, especially the ones with higher exposure to low-end devices. Despite this, Xiaomi, OPPO and vivo largely retained their market positions this quarter, with only marginal share losses.

Samsung reclaimed the top position in Q1 2026, primarily due to strong demand for the new Galaxy S26 Ultra. This led to a 3.6% YoY increase in shipments compared to the previous year, despite the later launch. The Ultra’s performance was enhanced by its consistent pricing compared to its predecessor. Additionally, the earlier release of the mid-range A-Series helped fill volume gaps from the S26’s later arrival and drive growth.

Apple secured second place, driven by the strong performance of the iPhone 17 series, which saw significant growth in China of over 30%. This led to a 3.3% year-over-year increase in global sales for Q1. Although demand remains robust, supply disruptions and a reduction in channel support in some key markets have hindered growth.

For the Chinese vendors, it was a mixed bag as some doubled down on their efforts in the Chinese market while others focused outside China amid the intense competition in the home market.

Xiaomi came in third for the quarter, maintaining its third position despite the steepest decline among the top five players, as it strategically reduced shipments of older models to avoid large scale price hikes.

OPPO placed fourth as it integrated with realme, with stronger performance in China than international markets helping offset a larger decline globally.

vivo achieved the fifth spot, closing its gap with OPPO on the global stage, driven by positive performance in China—its largest market—and maintaining leadership position in India.

Outside the Top 5, companies like Honor, Lenovo (Motorola) and Huawei also saw positive growth with Honor having the highest amongst the Top 10 of 24% YoY, as it shifted focus to overseas expansion.

How is the Smartphone Market Adapting?

“This was a challenging quarter for all smartphone players as they figure out a balance between profitability and growth and stabilization within home markets vs overseas expansion amid the constrained supplies and price pressure. Apple and Samsung benefited from their dominance in the premium segment where they strategically held back price increases, while others such as Xiaomi, OPPO, and vivo made concerted efforts to shift share to higher price bands,” said Kiranjeet Kaur, associate director of Consumer Devices, IDC. “Their resilience will continue to be tested over the next few quarters as they optimize and streamline their portfolio and respond with agility to market and supply chain changes. The strong footprint they had in Asia will be challenged as the low-end segment is eroded due to the price increases while expansion in Europe will face increasing competition from Apple and Samsung.”

What is the Market Outlook?

“The 4% decline in the market is just a sample of what’s to come as the memory situation intensifies on all fronts,” said Anthony Scarsella, research director for Mobile Phones, IDC. “Developed markets like the US that focus on premium models and with incentives such as trade-in and financing will be less susceptible to the overall impact of price increases. However, emerging markets that focus on sub-$200 devices will offer consumers very few options as the growing cost of memory components will represent a larger challenge than what the pandemic delivered over five years ago.”

Despite the negative shipment outlook, the market is moving towards higher ASPs due to rising costs and strategic shifts in vendor portfolios towards higher product mix. The premiumization trend will continue even as the memory prices are expected to stabilize by the second half of 2027.

To learn more, visit: www.idc.com