Worldwide Server Market Revenue Increased 61% During the Third Quarter of 2025 – IDC – January 7, 2026.

According to the International Data Corporation (IDC) Worldwide Quarterly Server Tracker, the server market reached a record $112.4 billion dollars in revenue during the third quarter of the year. This quarter showed another high double digit-growth rate by reaching a year-over-year (YoY) increase of 61% in vendor revenue compared to the same quarter of 2024.

Revenue generated from x86 servers increased 32.8% in 2025Q3 to $76.3 billion while Non-x86 servers increased 192.7% YoY to $36.2 billion.

Revenue for servers with an embedded GPU in the third quarter of 2025 grew 49.4% year-over-year representing more than half of the server market revenue. The fast pace at which hyperscalers and cloud service providers have been adopting servers with embedded GPUs has fueled the server market growth which almost doubled in size compared to 2024 with revenue of $314.2 billion dollars for the first three quarters of 2025.

“IDC expects AI adoption keep growing at an outstanding pace as major vendors continue reporting record orders and showing strong backlogs. Hyperscalers and cloud providers are still ahead with new, large deployments that require much higher compute density. Additionally, we started to see major AI based Research and Education projects that will help fuel further growth path in the market,” said Juan Seminara, research director, Worldwide Enterprise Infrastructure Trackers.

Server Regional Market Results

The United States is the fastest growing region in the server market with an increase of 79.1% compared to the third quarter of 2024, fueled by a 105.5% growth in the accelerated server segment. Canada grew 69.8% pushed by the same reason. PRC is growing at 37.6% year-over-year growth in 2025Q3 accounting for almost a fifth of the quarterly revenue worldwide. APeJC, EMEA and Japan also showed very healthy doble digit growth with 37,4%, 31.0% and 28,1% respectively, while Latin America showed a low single digit growth with 4.1% increase in the quarter.

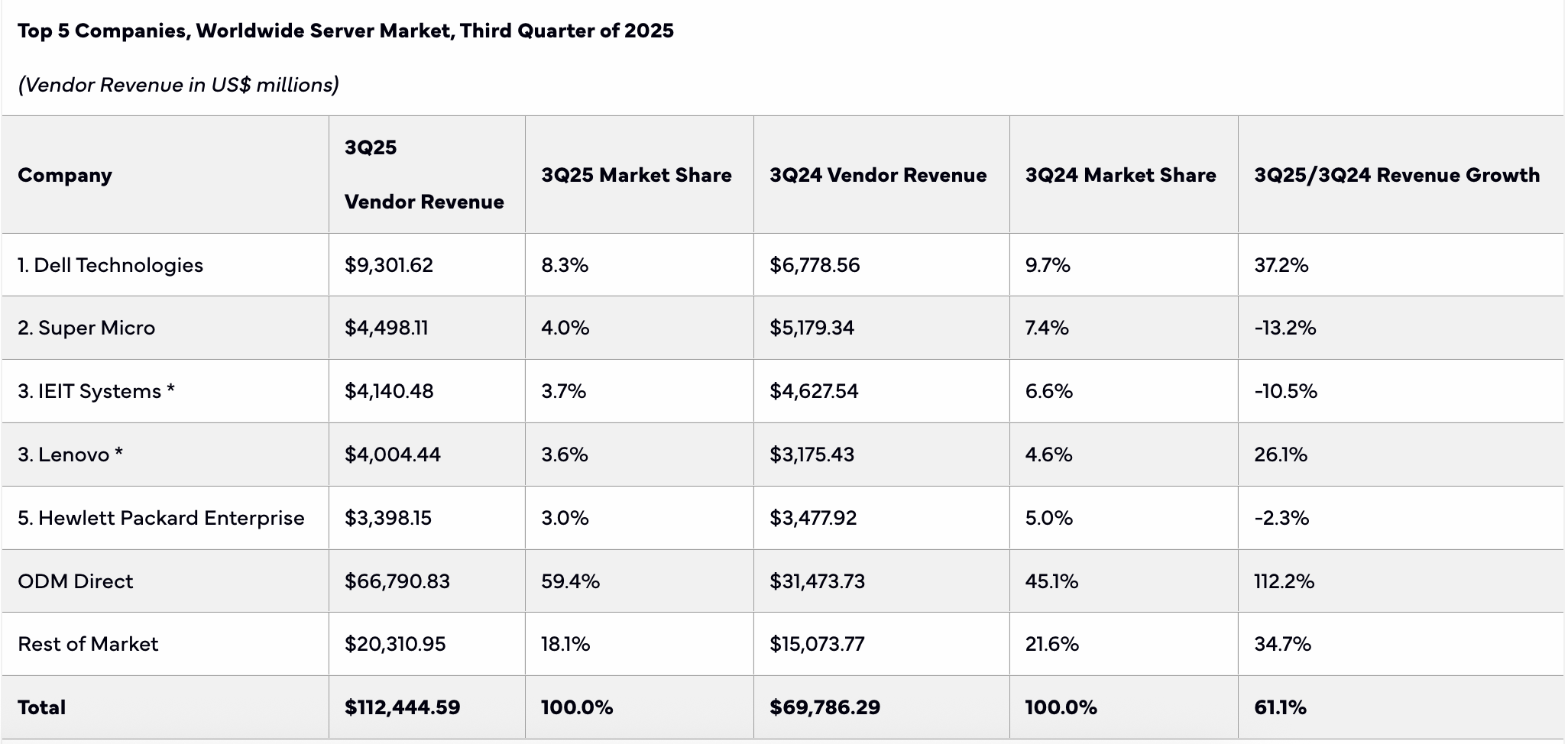

Overall Server Market Standings, by Company

Dell Technologies clearly lead the OEM market with 8.3% revenue share thanks to an outstanding growth on accelerated servers, Supermicro reached the second place with 4.0% revenue share even though declining 13.2% compared to 2024Q3. IEIT Systems and Lenovo statistically tied* for the third position in the market with 3.7% and 3.6% share respectively while Hewlett Packard Enterprise finished in the fifth position in the market, with 3.0% share.

IDC's Worldwide Quarterly Server Tracker greatly enhances clients' ability to respond quickly and effectively to today's dynamic server market. This product provides insight into customer trends by delivering geography-specific market size, market share, and market forecast details across all server segments. This IDC tracker product delivers a quarterly web database that details the performance of the market's individual players, and it answers important product-planning and product-positioning questions. This Tracker is part of the Worldwide Quarterly Enterprise Infrastructure Tracker, which provides a holistic total addressable market view of the four key enabling infrastructure technologies for the datacenter (servers, external enterprise storage systems, and purpose-built appliances: HCI and PBBA).

Taxonomy Notes

IDC defines a server system as a multiuser computing device that accesses and delivers services via a network. The server and the applications that run on it are typically shared by multiple users. Unlike a client device, a server does not usually have a user interface that is intended for human-machine interaction. A typical server system entails one or more processors, a motherboard, memory, internal disk or flash storage, a bundled operating system (OS), power supply units, and network interfaces.

Accelerator Type Definitions

Non-accelerated: These servers do not have an embedded accelerator. Servers where the accelerator is added by end users that have purchased the acceleration technology directly from an acceleration vendor and have installed it themselves are considered non-accelerated in IDC's Server Tracker. Servers with an integrated graphics processor (IGP) (i.e., fused to the motherboard) are also considered non-accelerated in IDC's Server Tracker.

GPU (Graphics processing units): A GPU is a processor specialized for rendering images, animations, or video to a computer display. In the context of server-based accelerated computing, a GPU is typically a programmable discrete (removable) graphics card but may also be an integrated graphics processor (i.e., fused to the motherboard). In addition to its graphical applications, a GPU may also be used to perform operations traditionally handled by a central processing unit, a concept known as a general-purpose graphics processing unit (GPGPU).

Other accelerated: This category combines servers with a discrete embedded accelerator FPGA or ASIC. In detail:

To learn more, visit: www.idc.com